From Alternative to Essential: The Expansion of Private Markets

January 14, 2026

Private markets — once the domain of large institutions and specialized investors — are now playing a central role in how businesses grow and how capital flows through the economy. As the global economy moves into 2026, private investment in companies, infrastructure, real estate, and credit are expanding rapidly, supported by convergence of public into private markets, technological change, and a new wave of industrial investment.

This growth reflects more than investor enthusiasm. Private markets are increasingly financing the real economy: building data centers, funding manufacturers, supporting logistics networks, and providing long-term capital to businesses that public markets struggle to serve. At the same time, access to private investments is broadening, bringing these markets closer to everyday investors.

Macro environment: stability, productivity, and reinvestment

Consumer spending remains resilient, and economic growth continues, albeit at a slower pace [1]. Inflation has moderated significantly, hovering below 3% [2]. Short-term interest rates are expected to trend downward, improving financing conditions and valuation clarity.

Labor markets show modest softening, driven largely by productivity gains from artificial intelligence rather than cyclical weakness [3]. AI adoption is enabling businesses to increase output with fewer incremental workers, supporting margins and encouraging capital investment.

More broadly, the economy is undergoing an industrial renaissance. Significant capital is being deployed across infrastructure, energy transition, data centers, defense, advanced manufacturing, and robotics. AI-driven growth is accelerating demand for both digital and energy infrastructure — sectors well suited for long-duration private capital. Demographic trends further support private markets as baby boomer retirements and private wealth growth drive demand for income-oriented and diversified investment solutions. Increased clarity around tariffs and trade policy has also reduced uncertainty, encouraging onshoring and domestic investment.

Private market momentum and capital formation

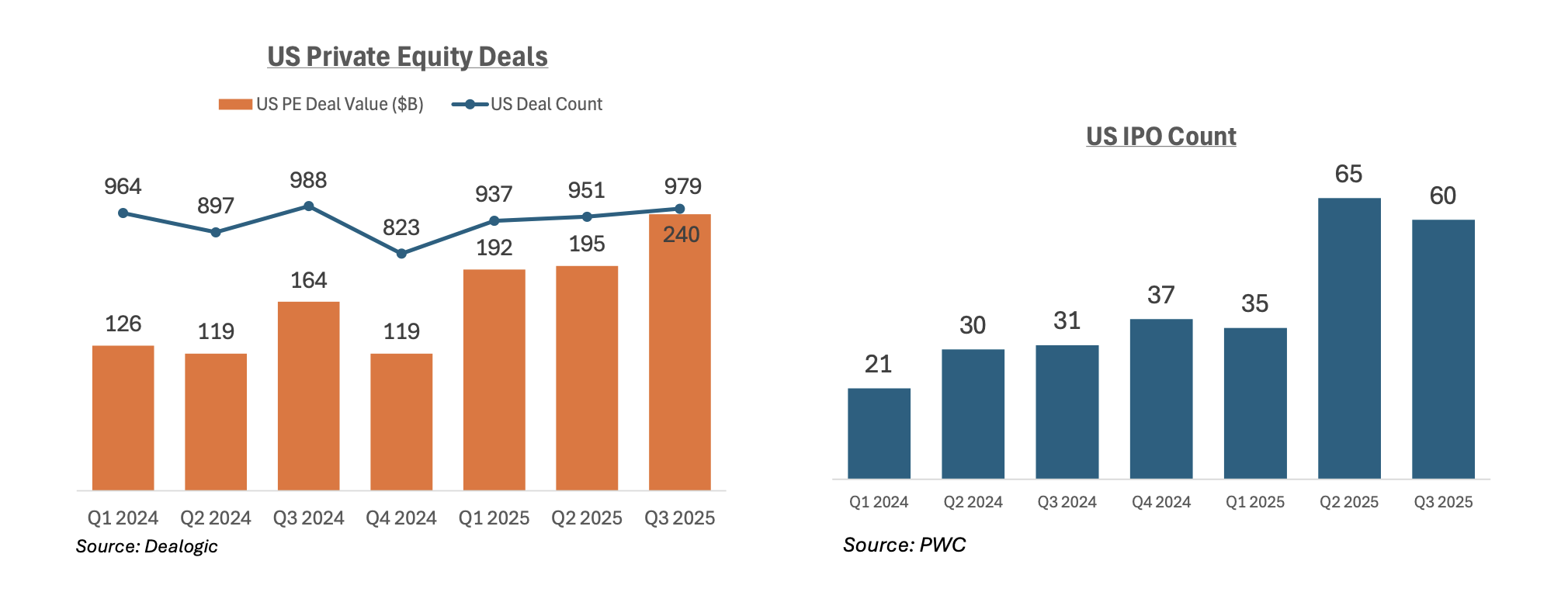

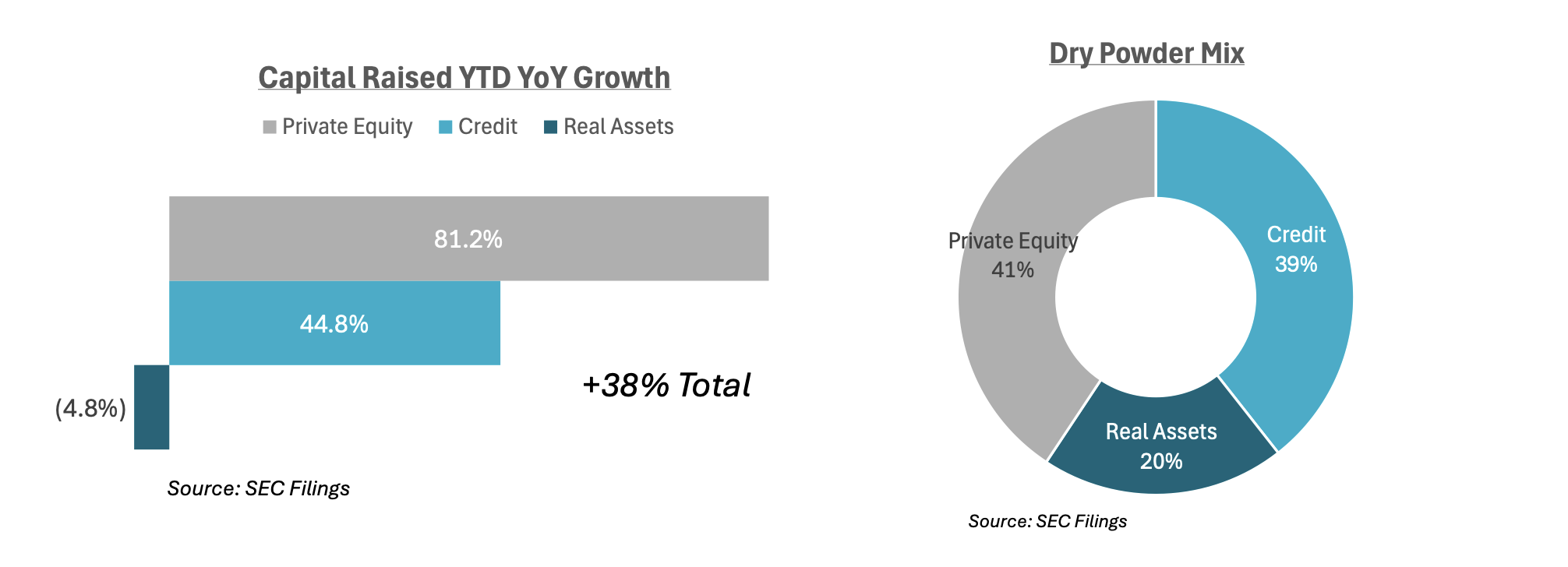

Investor demand for private markets remains strong with fundraising increasing approximately 38% year over year

Investor demand for private markets remains strong with fundraising increasing approximately 38% year over year [4], supported by improving confidence in transaction markets. M&A activity has rebounded, with larger transactions and a pickup in IPOs signaling healthier exit conditions. Dry powder grew 15% from the prior year, providing substantial capacity to invest across cycles [4].

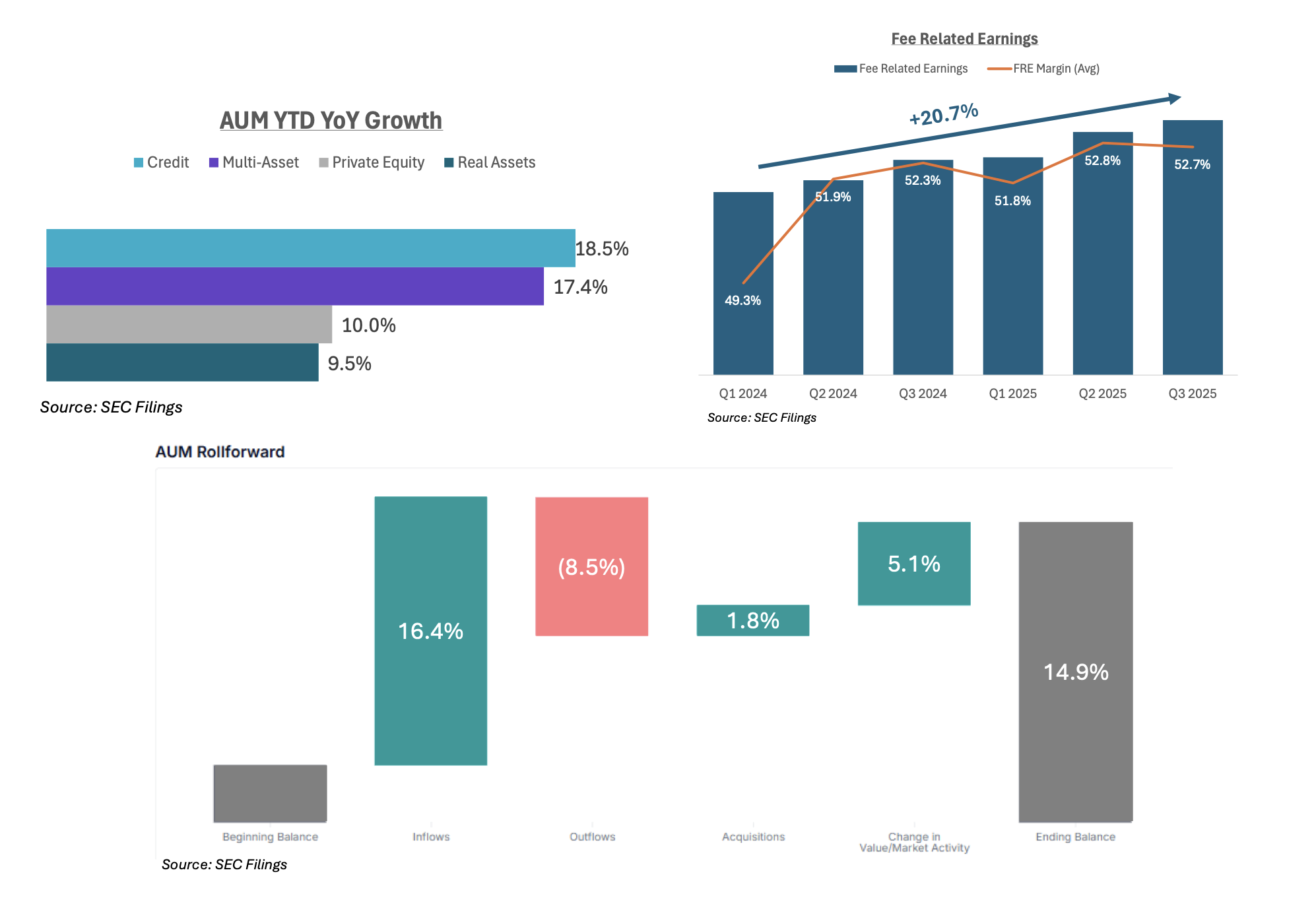

Assets under management continue to grow across strategies, with credit and multi-asset platforms leading. Inflows outpaced outflows by nearly two to one, while acquisitions increased 56% year over year, primarily in real assets. Fee-related earnings grew roughly 20.7% year over year, and management fees expanded at double-digit rates for most firms, led by strong growth at Blue Owl (+30% YoY)

Assets under management continue to grow across strategies, with credit and multi-asset platforms leading. Inflows outpaced outflows by nearly two to one, while acquisitions increased 56% year over year, primarily in real assets. Fee-related earnings grew roughly 20.7% year over year, and management fees expanded at double-digit rates for most firms, led by strong growth at Blue Owl (+30% YoY) [4].

Returns remain competitive, with private equity modestly outperforming credit, and real assets lagging

Returns remain competitive, with private equity modestly outperforming credit, and real assets lagging [4] but positioned for recovery as valuations stabilize, partially reflecting expectations of further interest rate declines.

Public-private convergence and channel expansion

A defining feature of today’s private markets is the expansion of access points, accelerating convergence with public markets, most notably demonstrated by the following:

- Private wealth individual investors looking to add private market investments to their portfolio where returns typically outpace public markets.

- Insurance platforms are increasingly important providers of perpetual capital, supporting long-duration credit and real asset strategies. Partnerships such as Blackstone–Legal & General and Blue Owl’s acquisition of Kuvare reflect this trend.

- Institutional investors are consolidating GP relationships, favoring top performing managers and companies offering comprehensive, multi-asset solutions.

- Traditional asset managers represent a large potential source of capital as private investments are embedded in mutual funds, ETFs, and structured products.

- Retirement channels may prove transformative. An executive order signed in August easing 401(k) restrictions on private market exposure — pending rule-making — signals a significant long-term opportunity. Early partnerships, such as Blue Owl with Voya Financial, highlight strategic positioning.

Together, these channels are broadening the investor base and reinforcing private markets as a core allocation.

Private credit

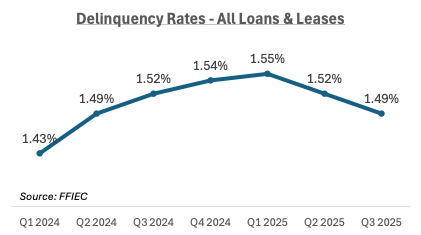

Private credit has become one of the fastest-growing areas within private markets. Credit quality remains solid as delinquencies are on the decline

Private credit has become one of the fastest-growing areas within private markets. Credit quality remains solid as delinquencies are on the decline [5]. While there has been an uptick in subprime auto lending defaults recently and the Tricolor and First Brands bankruptcies were isolated incidents related to fraud (bank-led and bank-syndicated led credit, not private credit), this is not a systemic risk to the private credit markets. Institutional demand for private investment-grade credit and semi-liquid products is growing. Core credit, ABF, and direct lending strategies are all seeing increased demand. ABF strategies are benefiting from collateral-based cash flows, inflation-adjustable pricing, and operational improvement opportunities. Despite its growth, direct lending totals approximately $1.7 trillion, relatively small compared to the $145 trillion global fixed-income market [6]. Increasingly, large corporations are turning to private credit for customized, long-duration financing which are difficult to replicate in the public markets.

Private equity

Private equity faces a more disciplined environment as institutional investors manage liquidity constraints and reduce the number of GP relationships. This favors large, differentiated platforms with strong sourcing, operational capabilities, and flexible capital solutions.

One standout investment strategy experiencing growth is Sports Capital. Firms are taking increasing interest in investing in Sports with Apollo Sports Capital (interest in Atletico de Madrid and Wrexham) and TPG Sports (partnering with Rory McIlroy and Sean O’Flaherty) launched this year along with Blue Owl’s GCP Strategic Capital Platform’s professional minority stakes strategy.

Real assets

Real assets are re-emerging as a growth area, particularly in residential, industrial, and data center sectors. Strategic acquisitions — such as Apollo’s purchase of Bridge Investment Group, Ares’ acquisition of GCP International, TPG’s acquisition of Peppertree Capital, and Blue Owl’s acquisitions of Prima and IPI and partnership with Qatar Investment Authority — underscore renewed conviction. Commercial real estate values appear to have bottomed in late 2023 and are recovering gradually. On the residential side, housing starts seem to have bottomed out with an expected slow, gradual recovery [7]. Long term demand for logistics and digital infrastructure remains strong, supported by e-commerce, AI, and energy needs. Recent examples of logistics include Ares consolidating under Marq Logistics and KKR launching Galaxy Container Solutions.

What this means for private markets

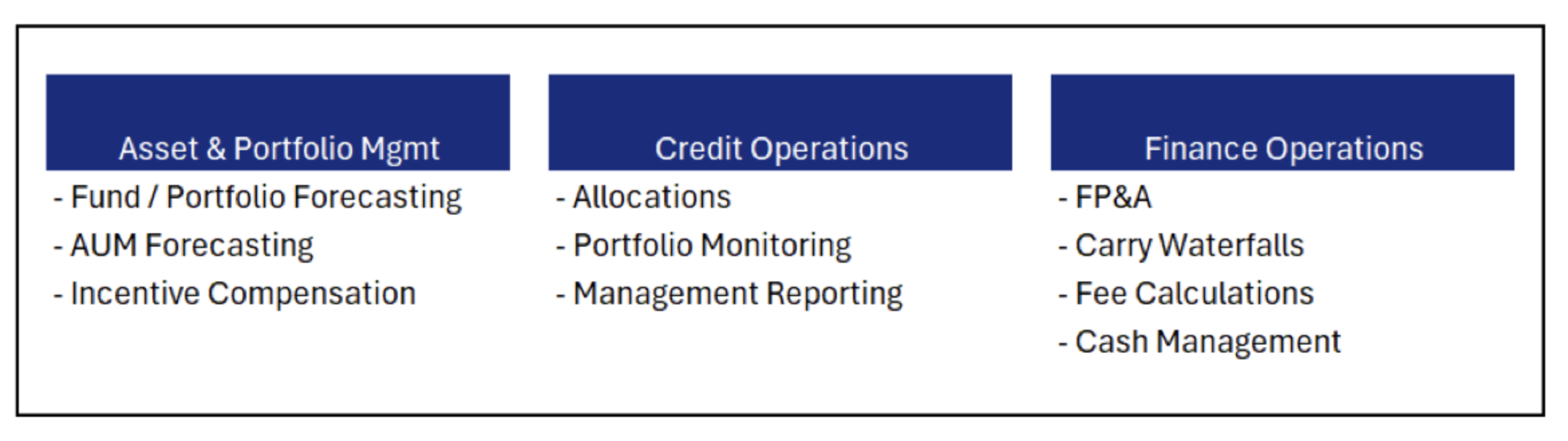

Private markets have evolved from alternatives to essential components of global capital markets. Channel expansion, increased investor demand, improved transaction environment, and macroeconomic AI and infrastructure headwinds have positioned this asset class for sustained growth. As companies in the private markets continue to grow, their planning needs have become more complex and require more scalable, actionable, and flexible solutions. From fundraising and deal management to portfolio and cash management, these companies are looking to operationally and strategically improve their planning processes. Over the past year, Alpha has worked with many of the major clients in the private markets space improving their planning capabilities. Some of the areas to highlight use cases are Asset & Portfolio Management, Credit Operations, and Finance Operations.

Questions? Email alts-info@alphafmc.com

Questions? Email alts-info@alphafmc.com

Sources

- Personal Consumption Expenditures and GDP (FRED)

- Inflation (BLS)

- Unemployment (BLS)

- SEC Filings

- Delinquencies (FFIEC)

- Direct Lending Market (KKR Q3 Earnings Call)

- Housing Starts (FRED) and Housing Expectations (Blackstone Q3 Earnings Call)